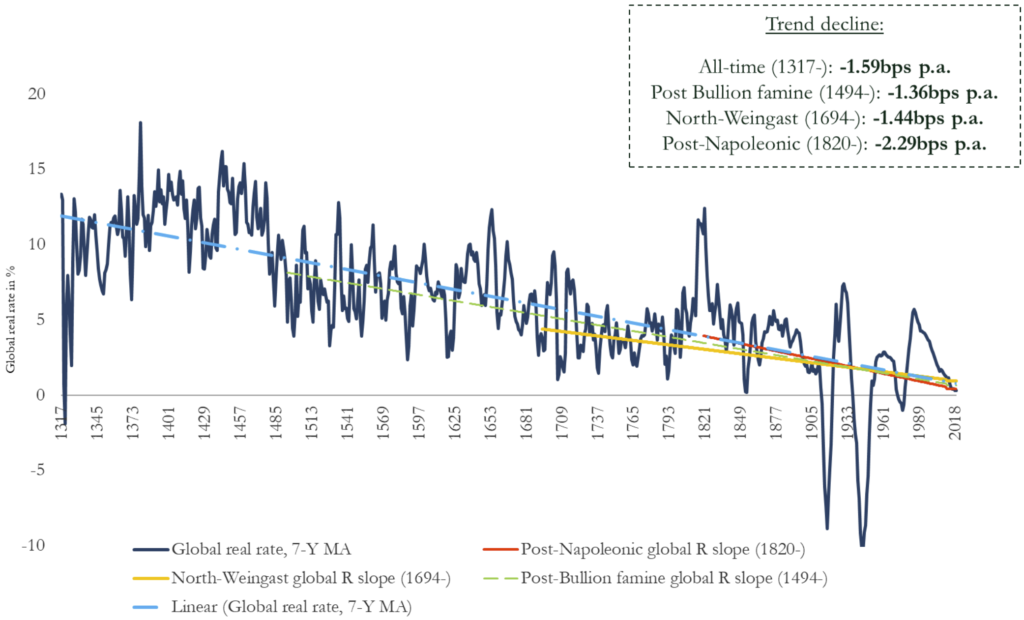

Headline global real rate, GDP-weighted, and trend declines, 1317-2018.

Here are excerpts from his conclusions:

First, my new data showed that long-term real rates – be it in the form of private debt, non-marketable loans, or the global sovereign “safe asset” – should always have been expected to hit “zero bounds” around the time of the late 20th and early 21st century, if put into long-term historical context. In fact, a meaningful – and growing – level of long-term real rates should have been expected to record negative levels. There is little unusual about the current low rate environment which the “secular stagnation” narrative attempts to display as an unusual aberration, linked to equally unusual trend-breaks in savings-investment balances, or productivity measures. To extent that such literature then posits particular policy remedies to address such alleged phenomena, it is found to be fully misleading: the trend fall in real rates has coincided with a steady long run uptick in public fiscal activity; and it has persisted across a variety of monetary regimes: fiat- and non-fiat, with and without the existence of public monetary institutions.

There is no reason, therefore, to expect rates to “plateau”, to suggest that “the global neutral rate may settle at around 1% over the medium to long run”, or to proclaim that “forecasts that the real rate will remain stuck at or below zero appear unwarranted” as some have suggested. With regards to policy, very low real rates can be expected to become a permanent and protracted monetary policy problem – but my evidence still does not support those that see an eventual return to “normalized” levels however defined : the long-term historical data suggests that, whatever the ultimate driver, or combination of drivers, the forces responsible have been indifferent to monetary or political regimes; they have kept exercising their pull on interest rate levels irrespective of the existence of central banks, (de jure) usury laws, or permanently higher public expenditures. They persisted in what amounted to early modern patrician plutocracies, as well as in modern democratic environments, in periods of low-level feudal Condottieri battles, and in those of professional, mechanized mass warfare.

I opine that this makes a lot of sense and leads me to think that a society where interest – and by extension inflation – are more-or-less non-existent, is possible.

We are already almost there; I receive no interest on money I deposit with a bank and last year Jsyke Bank in Denmark was peddling mortgages at minus 0.5%.

Economists (who, statistically, are more often wrong than right) will argue that a certain amount of inflation is necessary, but without providing undisputed evidence. The advantages and pitfalls of inflation are well-known and I personally find the concept of my savings automatically diminishing is abhorrent, but the clincher for me is that inflation is unsustainable.

For the past decade, monetary institutions have been pouring money into the world, following the economic ‘theory’ that this would jump-start economies and bring back the beloved inflation. These central bankers, in their arrogance, haven’t paused to consider the law of unintended consequences; their money-pouring has brought about:

Companies in poor health, which should have fallen by the wayside, are propped-up by virtually costless borrowing.

Banks are chastised for handing out too many mortgages by the very monetary authority which gave them the money to lend in the first place.

Rather than lending to businesses, the banks have used cheap money to bolster their balance sheets.

Inflation hasn’t risen and it never will in a society awash with money.

I sincerely hope that Schmelzing is right, the world will be a much more pleasant and stable place to live.

Planning retirement finances is harrowing; finding reliable, disinterested information is difficult. This paper studies and constructs a portfolio based on a set of formal requirements and analyses its potential performance by back-testing on 20 years of history.

Given a single down-payment, construct a portfolio that will generate a retirement pension. A stipend will be withdrawn the beginning of each year. The amount will increase by 1.3% p/a to compensate for the average inflation in Switzerland. The portfolio’s life shall exceed 30 years.

Objectives

The risk of total loss is minimised.

The portfolio shall be as resilient as possible to market turmoil.

Constraints

Instruments. Given the problem statement, the only viable instrument is shares.

Bonds cannot produce the required revenue.

Derivatives are subject to default by the writer.

Funds have a risk of default by the managing entity and their performance is predicated by fees.

Real-estate companies (as opposed to funds) that actually possess all their properties are acceptable because they are backed with physical property.

Currency. CHF only; forex risks are unacceptable because every currency has lost value against the Swiss Franc in the last 20 years.

Geography. The shares shall be in Swiss companies domiciled in Switzerland.

Debtor Diversity: No single company shall represent more than 5% of the portfolio.

Industry Diversity: No single industry shall represent more than 5% of the portfolio.

Deliverables

A set of objective criteria for stock picking that fulfils the constraints.

Based on these criteria, a basket of desirable shares in which to invest.

Buying, re-balancing and selling strategies.

An estimate of the stipend percentage range.

An analysis of the basket’s performance, by back-testing on historical data 2000-2019, which will determine:

The buffer that needs to be kept to maintain yearly payments, so as not to be obliged to sell at an unfavourable moment.

The portfolio’s probable behaviour in worst-case scenarios (e.g. entering the market just before a stock-market crash).

Situations in which the portfolio’s life might be compromised and mitigating actions.

Selection Criteria

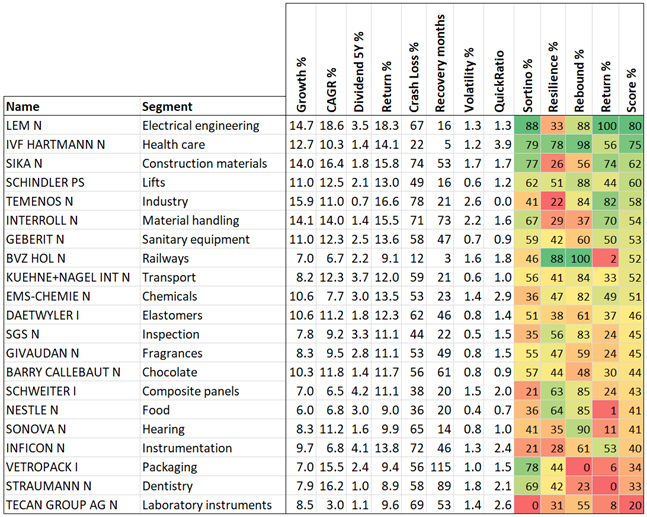

An ideal company would have a healthy balance sheet, exhibit constant growth and lose no value during a stock-market crash. Such companies do not exist, however amongst the 40-odd financial ratios available, 3 are particularly useful to filter out desirable candidates.

The Sortino ratio, a downside variant of the Sharpe ratio, is a strong predictor of companies that have the desired kind of behaviour.

The Quick Ratio, whilst dependent on the industry, generally demonstrates that a company has had the foresight to keep enough cash on hand to weather difficulties.

Resistance to turmoil, which can be assessed by observing the stock’s behaviour during a stock-market crash. It consists of two associated components:

Resilience. The percentage value remaining after a crash.

Recovery. The period of time before the stock re-attains its pre-crash value.

Graphically:

Ideal shares will have a resilience close to 100% and a short recovery.

(This graph is in fact the SPI and there were two major crashes. The latter is used as it is more recent. Thus, the SPI has a resilience of 47% and a recovery of 23 months).

Stock Selection

An initial selection is performed where companies will be scored using a decision matrix with 4 components outlined above:

The Sortinoratio, weight 20%.

The Resilience, weight 30%.

The Recovery, weight 30%.

The Return (growth plus dividend), weight 20%.

Note: The gold standard for expressing portfolio returns is the CAGR (Compound Average Growth Rate) but as it is calculated using solely a start and ending value, it is sensitive to the end-points:

This extreme case has a CAGR of -0.1% (the blue line) but over the entire period its global trend is positive (the green line, a least-squares linear fit).

Shares’ growths will be measured using the slope of the green line, expressed as a percentage of the average value, in this example 12%. The CAGR will also be calculated and used as a cross-check for cases like this.

From this subset a manual review will determine the companies finally chosen (judgement is required for the Quick Ratio, which has different meanings for each industry).

Universe

The initial instrument universe is the SPI and Swiss Real-Estate companies. Of the 215 SPI shares, 205 are quoted in CHF and totally domiciled in Switzerland. Of these, 82 and have been quoted continuously since 2000 and show positive returns.

Duplicate shares (e.g. Lindt N and Lindt PS) are be eliminated by the lowest score.

To meet the diversity constraint, a single stock with the best score of each industry segment is retained.

Selected shares

After applying the criteria and manual selection 21 shares remain:

These will constitute the proposed portfolio. The benchmark is the SPI.

Rejects

The remaining shares were eliminated because:

Railways. Despite their high scores, TITL BN BERG and JUNGFRAUBAHN HLD both have their entire infrastructure in one location. They were dropped in favour of BVZ HOLDING, which is significantly more diversified.

Foods. NESTLE scored lower but was preferred over BELL AG, which is not entirely Swiss and focussed on a single product line, meat. GROUP MINOTERIES has poor returns.

Chocolates. BARRY CALLEBAUT has a slight edge over LINDT and VILLARS.

The remainder due to insufficient resilience and/or recovery.

Weighting

The SPI index components are weighted by companies’ market value, as the aim is to assess the performance of the total CHF amount invested in the market.

On the other hand, an investor’s components are chosen to diversify risk; it is thus undesirable to give more weight to any particular company as this would proportionally increase risk for that component. Consequently, the portfolio will be built with equal CHF amounts of each stock.

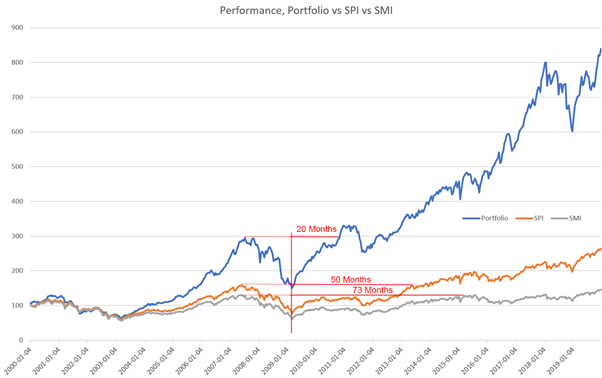

Performance Analysis

The baseline comparison consists of comparing the portfolio against the SPI and SMI, normalised to 100 on the 1st of January 2000:

Despite the impression due to the scale, all three lost ~55% in the 2007-2008 crash.

The portfolio recovers much faster (20 months), than the SPI (50 months) or the SMI (73 months).

Note: The SPI’s CAGR over the last 30 years is 9.89%.

Buffering

Selling shares to obtain cash for stipends is undesirable after a stock market crash, as their value will be down by some 55%. There is thus a requirement for a cash buffer to avoid such sales.

The portfolio recovers from a crash in some 20 months. Assuming that a stock-market crash occurs about once a decade, there will be two or three stock market crashes during the portfolio’s lifetime.

As the first crash can occur at inception, the minimum buffer is 2 year’s stipends. Assuming that the stipend is low enough to allow the portfolio to grow during the first half of its life, it may not be necessary to buffer for subsequent crashes.

Buffering with cash is costly with the current -0.7% negative interest. An attractive alternative is to use Real-Estate, which offers more modest growth but suffers much less in troubled markets. Of the 31 Real-Estate companies quoted on SWX, only 5 meet the criteria:

Their worst-case behaviour is a loss of ~15% and a recovery of 11 months, which is an acceptable level of risk given their average growth of 6.6%. (A 15% loss is covered by growth if the first crash occurs no earlier than 27 months after inception.)

This buffering strategy will be tested in the simulation.

Buying, Re-balancing and Selling strategies

Buying

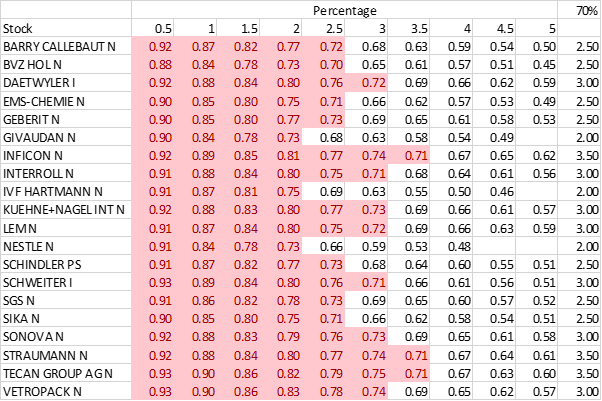

Of the 116’213 price changes of the members of the portfolio in the past 20 years, the average change was +0.0056 CHF. It follows that given the choice of buying today or waiting until tomorrow in the hope that the price will go down, it is logical to buy today (with an appropriate limit to avoid getting executed ‘high’ in the day).

This can by improved by observing a stock’s historical random walk to determine the chances of buying at a lower price over some period. For a given stock, for each day in the history, determine how often a price fall of at least X% occurred in the N following days (here, N=60):

Thus, if I want to buy Barry Callebaut, there is a 72% chance that it will fall by 2.5% in the next 60 days. Intuitively, sought-after shares (Givaudin, IVF Hartmann and Nestlé) are less likely to fall, so the limited order will need to be closer to the current price. Conversely, more volatile shares (Straumann and Tecan) are more likely to be had at a larger discount.

The buying strategy is thus to place limited orders at a discount of the percentage which meets the chosen chance of success. I implemented this strategy on the 2nd of October 2020. On the 20th of November, I had acquired 19 out of the 20 stocks at an average discount of 2.3% below the October 2nd prices, so this strategy works (except for Kühne & Nagel, which never fell 3% during the period).

Re-Balancing

The average cost of a transaction is about 0.85%, so the re-balancing cost is 1.7% of the position. This churning must be weighed against the hypothetical gain obtained by improved diversification.

It makes more sense to sell smaller fractions of multiple positions rather than entire positions, as the difference in transaction fees is negligible (0.825% for transactions over 50’000 versus 0.9% for those below 50’000).

Selling

The stipend pay-out will be made each year, using the dividends and sales as necessary. The simulations determined that the optimal rules for selling are:

When the market has fallen over the preceding year, prefer to sell real-estate otherwise sell shares (avoid selling shares at a poor price).

Select the 5 shares that have the highest growth in the last 12 months (5 was determined empirically).

Choose the two largest CHF positions.

Sell half the necessary amount of each of the two positions (to minimise unbalancing).

If a sale would represent more than 90% of the position, sell the entire position (to avoid subsequent odd-lot trades.

Simulation

A simulator was built to perform the back-testing. It operates as follows:

The simulation is initiated by:

Setting the clock to the start date.

Depositing CHF 1’000’000 in the account.

Immediately paying the stipend, proportional to the time remaining in the current year.

Use the remaining cash to populate the portfolio with shares and real-estate.

Then, repeatedly:

Advance the clock to 31st of December.

Calculate the dividends from the current positions and remove 35% withholding tax (which is written off). Credit the portfolio cash with the remaining 65%.

Pay-out custodian fees of 0.35% of the portfolio’s current market value.

Advance to 1st of January.

Increase the stipend by the rate of inflation.

Sell a sufficient amount of positions to make the cash greater than the current stipend.

Pay-out the stipend (or declare failure if there is insufficient cash).

Finally, calculate the P&L and various statistics.

Transaction fees are applied at the rates for UBS Online Banking. The rate varies by transaction size, about 0.85%. Other brokers / custodians charge significantly less.

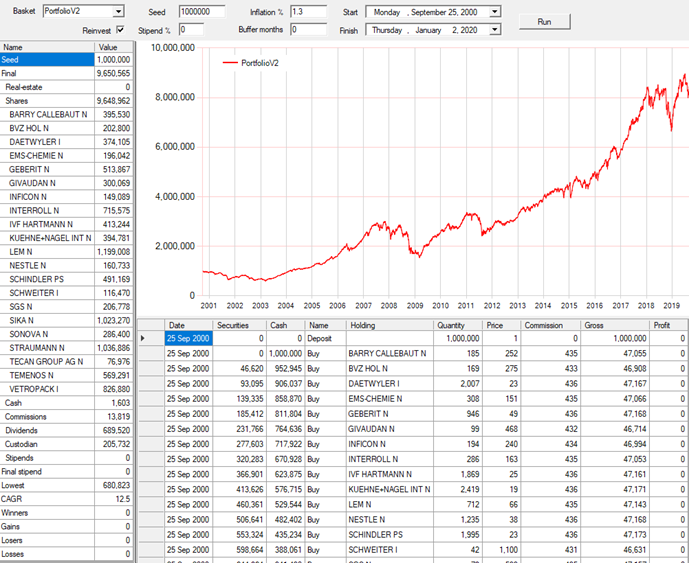

This is a worst-case, the 2000 stock-market crash commenced on the 25th of September 2000. The other worst case, starting on the 15th of October 2007, produces almost identical results.

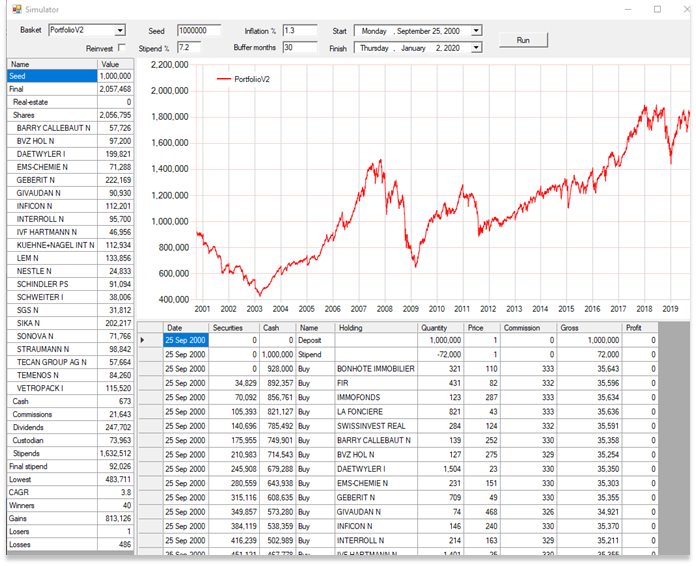

The stipend is 7.2%, CHF 72’000 on the first year, increasing to 92’026 after 20 years.

There are practically no sales at a loss.

The portfolio’s costs are 95’606 ÷ 20 years = 4’780 per year = ~0.5%. This could be significantly reduced by using a less expensive broker / custodian, e.g. SwissQuote.

The total stipends amount to 1’632’512 for an initial investment of 1’000’000.

The portfolio’s final value is just over double the initial deposit.

The portfolio has a CAGR of 3.8%, despite the stipend withdrawals.

The asset allocation remains moderately well balanced at the end of the simulation, the 21 initial companies all remain.

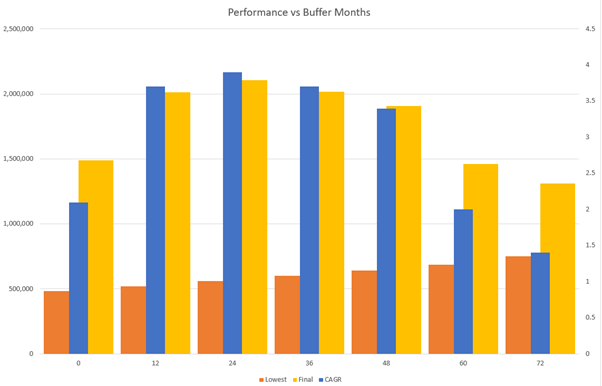

Determining the ideal buffer

Simulations were performed for varying buffer sizes from 0 to 6 years. Whilst increasing the buffer has a positive effect on the portfolio’s lowest value, the final portfolio value and the CAGR are affected negatively. It transpires that a buffer of ~30 months is optimal:

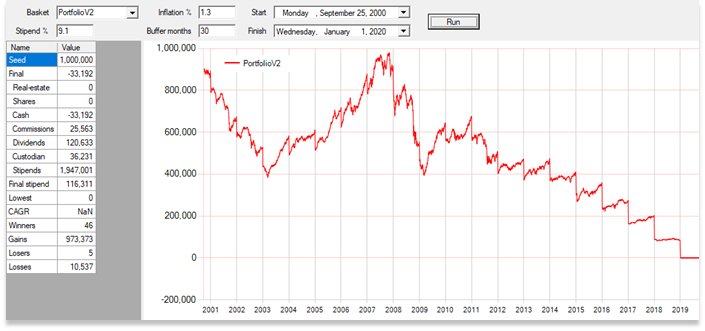

Maximum stipend

The portfolio fails (again, starting on worst-case 25/9/2000) at a stipend of 9.1%:

Ideal stipend

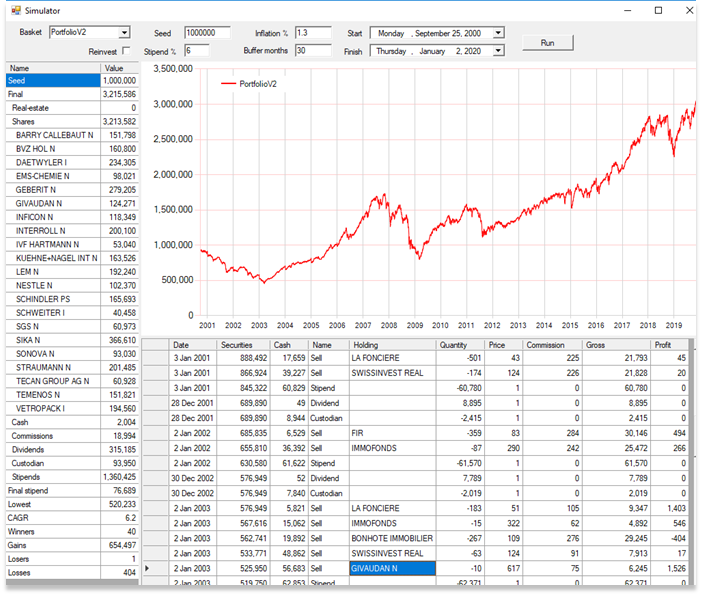

The chosen stipend is a function of the investor’s appetite for risk. With a stipend of 7.2% (the typical simulation above), the portfolio final value was 2’056’468 with a CAGR of 3.8%.

Decreasing the stipend to a more conservative 6% increases the final value to well over 3’000’000 with a CAGR of 6.2%:

Observe the transactions after the 2000 stock-market crash, where real-estate buffer is sold rather than stocks, until 2003 with the Givaudan sale.

Unfavourable situations

It is well-known that past performance is not a predictor for the future and a simultaneous stock-market and real-estate crash remains possible. Unforeseeable black-swan events will certainly happen in the incoming 30 years.

That said, most of the selected companies are manufacturers that have an established niche, producing tangible goods. All have a healthy balance sheet and have been well-managed for decades; the risk of total loss is thus extremely small.

Conclusion

The designed portfolio, implemented with a buffer of 30 months and a stipend of 6% meets the requirements with minimal risk.

Post-Scriptum

The same portfolio, run with neither stipends nor buffering and re-investing the dividends, starting on the pre-crash worst-case in September 2000, has the following behaviour (a CAGR of 12.5%):

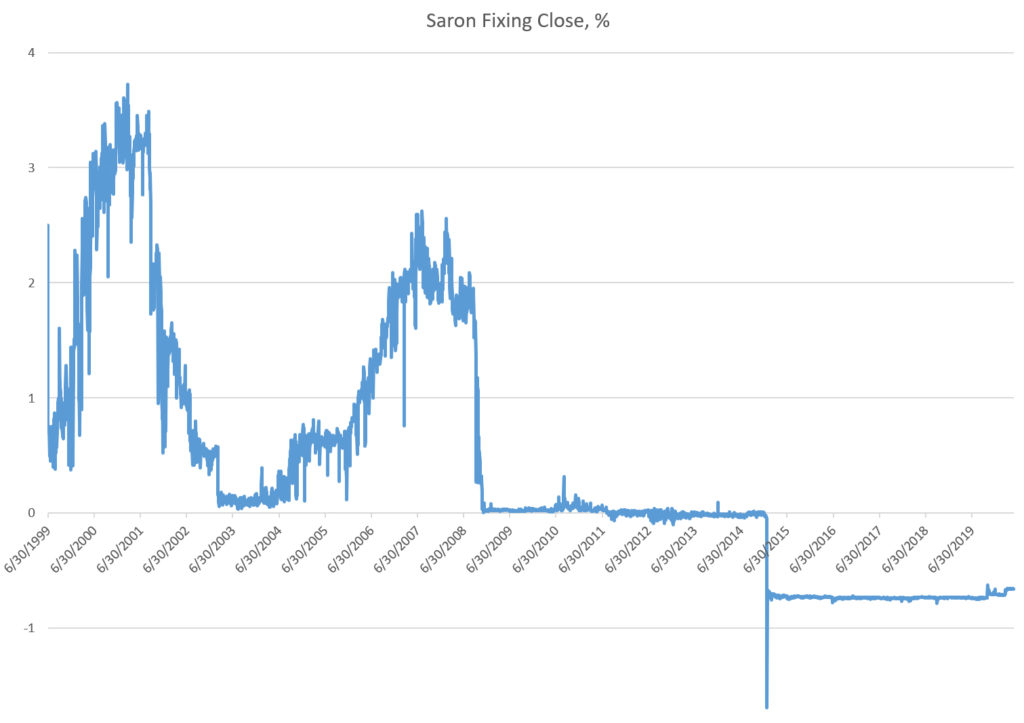

Back in 2011 the banks, many of them in the UK, were caught cheating by incorrect fixing the LIBOR rates between themselves. The British Financial Supervisory Authority was obliged to stop this and decided that the LIBOR would be abolished at the end of 2021 (it would apparently have been too much of a hardship to ask banks to stop fleecing the market immediately).

The Swiss National Bank had to invent an alternative to the LIBOR, which they did by creating the Saron (Swiss Average Rate Overnight), which isn’t based on rates that banks submit, but the true rate observed every day on the open market. These rates are publicly visible, so cheating is impossible (at least until banks find a novel way to cheat).

Said rates have been known since time immemorial and SIX (the Swiss Stock Exchange) provide a spreadsheet to calculate the Saron rate for any period since 1999. The Saron rates look like this:

Since mid-2015 the interest rate on the Swiss Franc has hovered around -0.7%. Notice that this a is a negative rate, which means that if “A” lends money to “B”, then “A” must pay “B” 0.7% for the privilege of lending him the money. Replace “A” with your bank’s name and “B” with your own name and re-read that sentence carefully.

Traditionally, banks have set LIBOR mortgage rates at about 1% over the interbank rate; their margin for the loan, fair enough. For the 1st of January to the 31st of March 2020, the Saron rate was minus 0.7058%. Adding the 1% margin, the mortgage rate should have been -0.7058% + 1% = 0.2942%.

During that period I paid 0.8% for my 3-month LIBOR mortgage. I have thus been over-charged 172% (0.8 is 172% of 0.2942).

(There is a minor, deliberate error in this. Can you spot it?)

Yesterday evening I was fortunate to be amongst a select few who had the privilege to be invited to hear the investment advice of the chief strategist of a major Swiss bank. (I should mention at the outset that the vast majority of the audience’s reference currency is the Swiss franc.)

The speaker was clearly an erudite man and his delivery was flawless. The underlying theme of his speech was divergence in today’s economy: in interest rates, in GDP, in unemployment, in central banks’ strategies, and so forth. Render unto Caesar, his presentation was concise, well-researched and extremely persuasive.

The conclusion of his argument was the bank’s investment strategy. In a nutshell, Swiss and European equities present few opportunites. On the other hand, the USA appears to have left recession and is showing strong growth perspectives, which he estimated at around 6%. The bank’s strategy is thus to move their clients’ assets to Swiss and European gilt of the highest quality for portfolio protection and to US blue-chips for revenue.

When questioned on the Swiss National Bank’s strategy of locking the Swiss franc to a floor of 1.20 CHF/EUR, he was of the opinion that the floor to the Euro would be replaced by a floor against a basket of currencies, probably EUR/USD/JPY, sometime in 2015.

Were I to have followed his advice, this morning, first thing, I would have moved my investments into US blue-chips, the stocks that participate in the Dow-Jones Index: American Express, Boeing, Caterpillar, etc. in the hope of a return of some 6% instead of the measly percent or two that I get on Swiss franc holdings.

With the most tragic timing for our strategist, some 14 hours later the Swiss National Bank announced that it had abandoned the 1.20 floor. The effect was instantaneous: the EUR and the USD crashed against the CHF, settling at day-end to ~0.86CHF/USD and CHF/EUR at a similar rate.

Had I bought those American shares some hours previously, I would have taken a 15% hit on my portfolio in so-many hours; even if the strategist’s predictions come true, I’ll have to wait two and a half years before breaking even.

There are several lessons to be learned from this story:

Despite everything that your banker, hand-on-heart, assures you, he has no interest whatsoever in your financial well-being. His sole aim in life is to persuade you to trade your holdings as often as possible so that he can gather a maximum commission. If, despite the commissions, you make money, he’ll congratulate himself on having helped you. If you lose money, he’ll appear heart-broken at your misfortune, which was entirely due to the unfavourable market.

If your reference currency is the CHF and you invest in higher-yield USD-labelled assets, you’re exposed to the CHF/USD exchange risk. Momentarily you might get away with it; as this example shows, you are likely to take a caning.

Inversely, if your reference currency is the EUR and you buy CHF assets, your yield will be much more frugal… but your capital will be better preserved.

The take-away from all this is that in today’s liquid markets there is no free lunch. If your ambition is to receive the rate of inflation plus a whisker on your investments, there’s a strong likelihood that you’ll get it. If your ambition is get 6%, be prepared to lose 15% momentarily when things go tits-up.

P.S. For those whose mother-tongue is not English, the title is a pun

18 months ago I suggested that UBS get out of investment banking, if for no other reason than I was sickened by having to pay thousands of francs to bail a too-big-to-fail greedy bunch of arseholes who should have been hung out to dry long ago. I apologise for the strong language, but I really am sick and tired of this. In an unexpected move, they appointed Sergio Ermotti, a wise Swiss-Italian (like the brilliant Alfredo Gysi) as group CEO and he had the sense wind down the loss-making division. I’m far from ready to heap praise on UBS, but let us render unto Caesar, it’s a step in the right direction.

The European Union has decided to bail out the Cypriots on the condition of imposing a 9.9% one-off tax on holdings over €100’000 deposits in Cypriot banks and 6.7% below €100’000. The justification is that Cyprus only represents 0.2% of the EU GDP and the holdings in question are held mostly by rich Russians and a handful of under-represented Brits. Be that true or not makes no difference; citizen X living in Cyprus has exactly the same rights as citizen X living in France, Germany or wherever. Unilaterally confiscating a citizen’s assets without due cause is not only unacceptable, it is theft. Were my government to propose such a measure, my instinctive reaction would be to buy a weapon; for if my basic property rights are no longer secure, there’s little left else to lose.

The European Union seems close to making a law that limits excessive bonuses. Few will disagree that the finance industry needs to be curbed, and the intention is good. The problem is in the method proposed; no matter how carefully it will be worded (the text apparently runs to over 1’000 pages), they’ll always be someone smarter to find a work-around.

The wiser and far more concise solution problem was proposed by the Swiss entrepreneur Thomas Minder in the initiative he made back in 2008. Here is an English translation, which I made from the official German and French texts:

Federal Peoples’ Initiative “against Rip-off”[1] The Swiss Federal constitution of 18 April 1994 is completed as follows:

Article 95, alinea 3 (new)

In order to protect the economy, private property and shareholders and to ensure sustainable management of businesses, the law requires that Swiss public companies listed on stock exchanges in Switzerland or abroad observe the following rules:

Each year, the Annual General Meeting votes the total remuneration (both monetary and in kind) of the Board, the Executive Board and the Advisory Board. Each year, the AGM elects the President of the Board or the Chairman of the Board and, one by one, the members of the board, the members of the Compensation Committee and the independent proxy voter or the independent representative. Pension funds vote in the interests of their policyholders and disclose how they voted. Shareholders may vote electronically at a distance; proxy voting by a member of the company or by a depositary is prohibited.

Board members receive no compensation on departure, or any other compensation, or any compensation in advance, any premium for acquisitions or sales of companies and cannot act as consultants or work for another company in the group. The management of the company cannot not be delegated to a legal entity.

The company statutes stipulate the amount of annuities, loans and credits to board members, bonus and participation plans and the number of external mandates, as well as the duration of the employment contract of members of the management.

Violation of the provisions set out in letters a to c above shall be sanctioned by imprisonment for up to three years and a fine of up to six years’ remuneration.

Article 197 chapter 8 (new)

Pending implementation of the law, the Federal Council shall implement legal provisions within one year following the acceptance of article 95 alinea 3.

The genius of Minder’s text is that instead of setting limits on bonuses, it simply forces shareholders to approve them every year, whilst ensuring that it’s the real shareholders that vote.

We’ll be voting on it this weekend (I already voted for) and it seems that it has a good chance of passing. If it does,

Minder’s text was passed on the 3rd of March 2013 by all the counties and an astonishing 67.9% of the voters. Of the 183 initiatives submitted to the vote in Switzerland since 1893, only 21 (8.7%) have been accepted. 67.9% is the 3rd highest score ever obtained by a popular initiative. The highest score, 83.8%, was obtained in the 1993 initiative to make the 1st of August a National holiday; hardly ground-breaking. The 2nd highest score, 71.4%, was for the 1921 initiative on international treaties.

I predict that the concept will gradually be adopted globally and Thomas Minder will be recognised as the father of a new era in corporate governance.

1. It is difficult to find an exact translation of Abzocker. Cheater, swindler, deceiver and liar are all close. Abzockerei literally means rip-off, but Abzockerei isn’t slang. Scam is another synonym.

So S&C get a huge fine for having traded with Iran. Naughty boys. In our capitalist society, nobody will question that banks are there to make money, which by definition is odourless. Punishing a bank for dealing with X is morally identical to punishing Smith and Wesson when a gun they manufactured is used to kill X. If a criminal steals a gold ingot and buries it, are you going to take the soil to court? Going after banks is no more than a short-cut to apprehending the criminal in the first place. Much easier of course, but fundamentally incorrect.

Lest I be misunderstood, I have not the least sympathy for bankers and their ilk, but “money-laundering” is a euphemism for “finding the criminal is too much effort”; there’s nothing wrong with looking after X’s money; if X got it illegally, then have him punished for his crime. Smith and Wesson anybody?

So UBS has lost $350M after Facebook’s botched launch, and the only people to be surprised are those who were stupid enough to try and buy the shares instead of buying puts (which would have made them significantly richer).

UBS is supposed to be one of the world’s leading banks, and yet time and again they squander money in a manner which beggars belief. I’d find it laughable if I hadn’t been forced to pay my taxes to provide UBS with a 65billion$ bailout a couple of years back; the way things are going it seems more than likely that they’ll be back, cap-in-hand, in the not-so-distant future.

What does surprise me is the naivety of all concerned. It appears that many well-paid employees at UBS subscribed to the idea of buying shares in a company whose business model is based solely on displaying advertisements which are completely ignored by a barely-literate proletariat bent on exchanging mindless drivel.

In a few years, Facebook will be remembered as an ugly skid-mark on the digital toilet.

Hopefully sooner, UBS will nominate a CEO who can learn from his predecessors’ mistakes: sell off the investment banking division, close all operations in the USA and focus on what the bank does well: private banking. The Swiss will once again be proud of their successful bank and grateful both for the reduction in taxes and hassles from the Americans.

Just before Christmas 2010 I gave my yearly prediction as to how I saw the forex market evolving.

Those that read it heaped ridicule on me: “the dollar couldn’t devalue, it’s unthinkable, it’s the world’s reserve currency, you’re crazy”, “the Euro could never fall like that”.

Six months down the road, let’s take a look at how things really turned out.

The red line (USD) and pink line (EUR) are those I drew last Christmas, the green ones are the current situation on the 22nd of June 2011 (1 CHF=0.8360 USD = 1.2030 EUR):