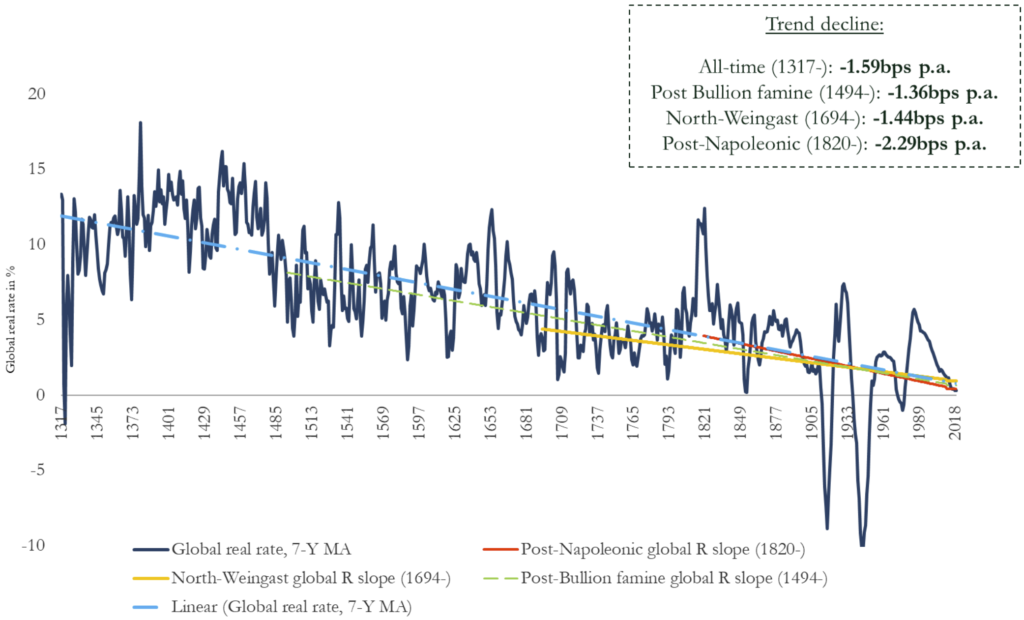

Paul Schmelzing at the Bank of England recently published a working paper “Eight centuries of global real interest rates, R-G, and the ‘suprasecular’ decline, 1311–2018” in which he argues, very persuasively, that both interest rates and their volatility have been steadily declining for the last 700 years.

This graph summarises his hypotheses:

Here are excerpts from his conclusions:

First, my new data showed that long-term real rates – be it in the form of private debt, non-marketable loans, or the global sovereign “safe asset” – should always have been expected to hit “zero bounds” around the time of the late 20th and early 21st century, if put into long-term historical context. In fact, a meaningful – and growing – level of long-term real rates should have been expected to record negative levels. There is little unusual about the current low rate environment which the “secular stagnation” narrative attempts to display as an unusual aberration, linked to equally unusual trend-breaks in savings-investment balances, or productivity measures. To extent that such literature then posits particular policy remedies to address such alleged phenomena, it is found to be fully misleading: the trend fall in real rates has coincided with a steady long run uptick in public fiscal activity; and it has persisted across a variety of monetary regimes: fiat- and non-fiat, with and without the existence of public monetary institutions.

There is no reason, therefore, to expect rates to “plateau”, to suggest that “the global neutral rate may settle at around 1% over the medium to long run”, or to proclaim that “forecasts that the real rate will remain stuck at or below zero appear unwarranted” as some have suggested. With regards to policy, very low real rates can be expected to become a permanent and protracted monetary policy problem – but my evidence still does not support those that see an eventual return to “normalized” levels however defined : the long-term historical data suggests that, whatever the ultimate driver, or combination of drivers, the forces responsible have been indifferent to monetary or political regimes; they have kept exercising their pull on interest rate levels irrespective of the existence of central banks, (de jure) usury laws, or permanently higher public expenditures. They persisted in what amounted to early modern patrician plutocracies, as well as in modern democratic environments, in periods of low-level feudal Condottieri battles, and in those of professional, mechanized mass warfare.

I opine that this makes a lot of sense and leads me to think that a society where interest – and by extension inflation – are more-or-less non-existent, is possible.

We are already almost there; I receive no interest on money I deposit with a bank and last year Jsyke Bank in Denmark was peddling mortgages at minus 0.5%.

Economists (who, statistically, are more often wrong than right) will argue that a certain amount of inflation is necessary, but without providing undisputed evidence. The advantages and pitfalls of inflation are well-known and I personally find the concept of my savings automatically diminishing is abhorrent, but the clincher for me is that inflation is unsustainable.

For the past decade, monetary institutions have been pouring money into the world, following the economic ‘theory’ that this would jump-start economies and bring back the beloved inflation. These central bankers, in their arrogance, haven’t paused to consider the law of unintended consequences; their money-pouring has brought about:

- Companies in poor health, which should have fallen by the wayside, are propped-up by virtually costless borrowing.

- Banks are chastised for handing out too many mortgages by the very monetary authority which gave them the money to lend in the first place.

- Rather than lending to businesses, the banks have used cheap money to bolster their balance sheets.

- Inflation hasn’t risen and it never will in a society awash with money.

I sincerely hope that Schmelzing is right, the world will be a much more pleasant and stable place to live.