Back in 2011 the banks, many of them in the UK, were caught cheating by incorrect fixing the LIBOR rates between themselves. The British Financial Supervisory Authority was obliged to stop this and decided that the LIBOR would be abolished at the end of 2021 (it would apparently have been too much of a hardship to ask banks to stop fleecing the market immediately).

The Swiss National Bank had to invent an alternative to the LIBOR, which they did by creating the Saron (Swiss Average Rate Overnight), which isn’t based on rates that banks submit, but the true rate observed every day on the open market. These rates are publicly visible, so cheating is impossible (at least until banks find a novel way to cheat).

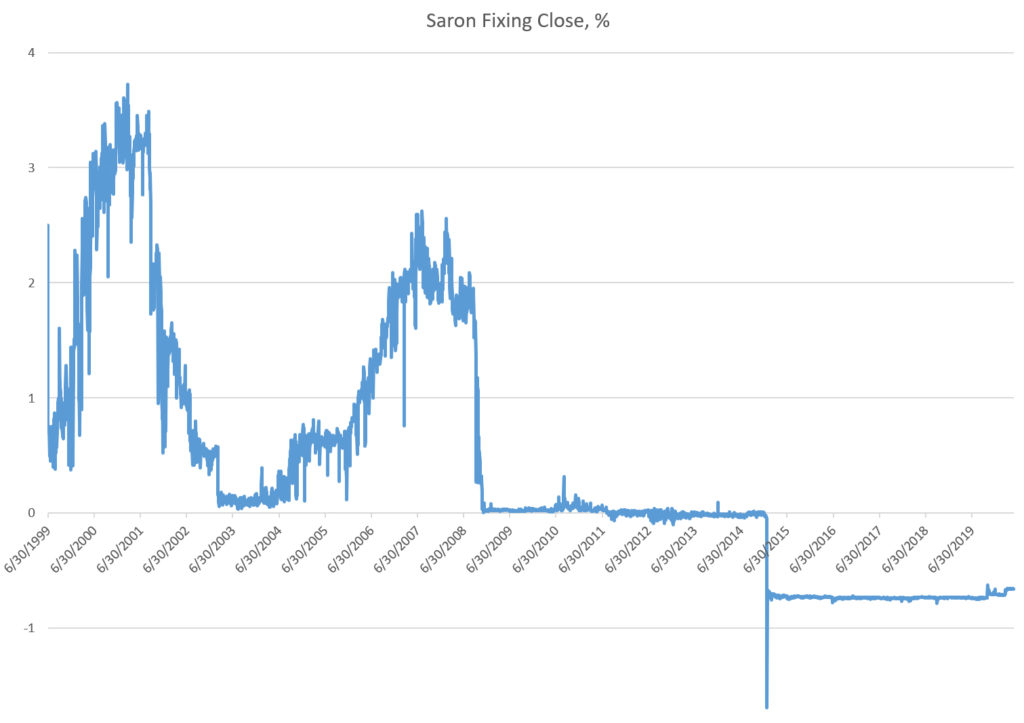

Said rates have been known since time immemorial and SIX (the Swiss Stock Exchange) provide a spreadsheet to calculate the Saron rate for any period since 1999. The Saron rates look like this:

Since mid-2015 the interest rate on the Swiss Franc has hovered around -0.7%. Notice that this a is a negative rate, which means that if “A” lends money to “B”, then “A” must pay “B” 0.7% for the privilege of lending him the money. Replace “A” with your bank’s name and “B” with your own name and re-read that sentence carefully.

Traditionally, banks have set LIBOR mortgage rates at about 1% over the interbank rate; their margin for the loan, fair enough. For the 1st of January to the 31st of March 2020, the Saron rate was minus 0.7058%. Adding the 1% margin, the mortgage rate should have been -0.7058% + 1% = 0.2942%.

During that period I paid 0.8% for my 3-month LIBOR mortgage. I have thus been over-charged 172% (0.8 is 172% of 0.2942).

(There is a minor, deliberate error in this. Can you spot it?)